How to make HDB housing affordable (Part 1)

My Proposed Solutions – Plan A

(This is a continuation of a previous post.)

This is based on the existing housing system and policies.

1. Fix the Valuation process. The current valuation system is as mentioned previously, a big part of what has caused housing prices to balloon.

Yes, the surveyors are independent from HDB, and should value the property value fairly. However, they should stop trying to include COV prices with every new valuation. How can a flat cost $15-$20k more in one month? It’s human nature to always want to sell your flat above valuation. That doesn’t mean that the flat’s value is such.

2. Raise the HDB income Ceiling. Doing this will allow more people to be eligible for HDB loans and housing grants. This would lower their down payment to 10%, and with the grants, this sum is more attainable. Furthermore, the only cash they have to fork out upfront is the COV. (Bank loans require 5% cash). On top of that, interest rates will be pretty steady at 2.6% per annum.

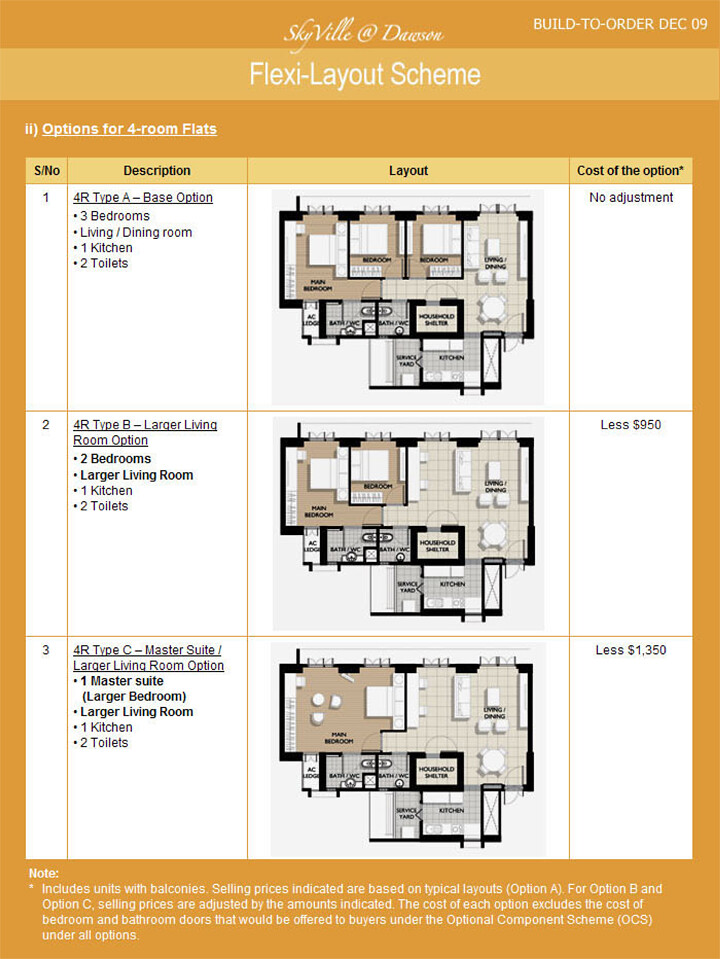

3. Come up with new kinds of flats. Actually, HDB already has shown some flexibility in this area. I viewed the Dawson floor plans some time back, and they allowed different configurations for their new 4-room flat.

3. Come up with new kinds of flats. Actually, HDB already has shown some flexibility in this area. I viewed the Dawson floor plans some time back, and they allowed different configurations for their new 4-room flat.You could choose to have 2 bedrooms and 1 larger living room (for when you do not yet have kids), and then subdivide an extra room out of the living room in the later part of life (for when you have 2 kids wanting their own rooms), or simply get rid of all the rooms except the master bedroom (for when your children have moved out, and now have kids, so that there’s more space for the extended family to mingle during visits).

My suggestion is a modification of the above – Let home owners have a home that can grow with them. Instead of selling a 4-room flat, package it in a 2+1 configuration – A 2 bedroom flat connected to a studio via a door in the middle which can be locked on both sides. (similar to the connecting doors in hotel rooms). Locking it creates 2 flats, while leaving it makes it a single unit. It takes up exactly the same floor area and has exactly the same number of toilets and room. The only difference is that it has two separate main entrances.

What’s the point of selling these kinds of flats? Refer to the diagram below, and consider the following:

- Stage 1 A young couple can choose to live in the studio first (yellow), and then rent out the 2 bedroom flat (brown). The rental can help pay for their mortgage + some extra cash*, and help them save money to start a family.

Stage 2 When their first kid comes along, they can then move to the 2 bedroom flat (brown), and then rent out the studio (yellow). Their rental income will decrease, but it’ll still help cover most of their mortgage, with the rest payable through CPF*, leaving them enough money to raise a family.

Stage 3 Another kid comes along, and soon their kids are old enough to have their own rooms. The studio (with the connecting door) can then be used as the master bedroom, and each kid can have their own room. At this point, there is no rental income. But by this time, the parents should have established their careers, and should earn enough.

Stage 4 The kids have grown up and have married. The nest feels empty now. The couple can then choose to retire in the studio (yellow), and rent out the 2 bedroom flat (brown). (Or live in the 2 bedroom flat and rent out the studio.) The rental becomes their ‘retirement income’.

In this way, the flat grows with the family’s needs, providing rental income to cover their mortgage when they first start out, and in old age, provides income for their retirement. At the same time, since not all their OA is used to pay for the flat, there is actually some money to contribute to the minimum sum.

Note that the above scenario does not take into account the fact that rental income will increase as the years go by.

With the Additional Housing Grants available, the lower income will also have the chance to get a 2+1 (4rm flat), and be able to service most of the mortgage with the rental. This beats limiting them to getting a 2-room flat, and then never being able to upgrade due to limited funds. Of course different flat configurations like 1+1 (3rm flat) or 2+2 (5rm flat) can also be offered to suit different income levels.

Some may question, “you can already rent out your spare rooms currently, so why divide the flat into 2 flats?” The answer is simply this: Privacy leads to higher rents. Room rentals only fetch about $500-$600k. And for this amount, you lose your privacy, you have to pay for their utility usage, and sometimes, they mess up your house or kitchen.

Besides, like I mentioned before, it’s still takes up the same space as an existing 4-room flat! I mean, if the Government intends to open the doors to foreigners, at least let the locals benefit in some way.

*Based on a 4room flat price of $350k, 30 year loan @ 2.6% interest - Monthly Installment = $1,261 - Current 2 bedroom flat rental = $1.5-$2k - Current 1 bedroom flat rental – $1.1k (based on 1 rental. It’ll probably be lower, at perhaps $800) - Figures based on HDB Website

And that’s the end of Plan A. Got to hit the sack. Need to work tomorrow. Check back tomorrow night for Plan B.

*Update* Plan B has been posted.

How to make HDB housing affordable (Part 2)

My Proposed Solutions – Plan B

This proposal tackles the issue of providing cost-plus low price housing without adversely affecting current HDB flat prices.

The current types of HDB available:

- Rental Flats – very cheap rental housing provided for poor and needy citizen families

Studio Apartments – only available for folks 55 years and above, and have a short lease of only 30 years.

Build-to-order (BTO) – 2/3/4/5 room flats make up the bulk of new flats, which a range of prices depending on the flat locations.

Design Build and Sell Scheme (DBSS) – they are essentially condo-like flats, and thus are more expensive than BTOs. Executive Condominiums (EC) – first created to allow the sandwiched class to get a condo (with full facilities), but at a lower prices. ECs are fully privatised after 10 years.

Most of the Opposition parties are proposing BTO flat prices to be slightly above cost or pegged to the median household income. Seeing how flat prices has ballooned by as much as 50% in less than a decade, selling flat prices at much lower prices will definitely affect recent flat owners. Some would be sitting on homes worth more than their loans when these flats enter the resale market in 8 years.

But with flat prices going up, and families having to take up 30 year loans just to pay it off, future generations might never be able to buy a place they can call home. So something definitely has to be done.

What if a new category of flats were to be created? Let’s call these flat “Type B” flats, while existing BTO flats shall be known as “Type A”.

Type B flats:

- - Should be pegged to median household incomes - Should be delinked from the market - When sold, price will be pegged to prevailing median household income - Can only be sold to other 1st time buyers or Type B upgraders/downgraders - Cannot be sold to PRs - Are meant solely for owner occupation, and whole units cannot be rented out (this is to prevent people for buying said flats for investment purposes) - Like rental flats, will be within current estates to prevent a division of classes - Only first timers or Type B upgraders/downgraders are eligible to purchase

Type B flats will be affordable, but owners will not “profit” from the sale of their flats, unlike Type A flats which is pegged to market prices.

Type B flat owners can choose to switch to Type A resale flats should they want to benefit from normal market prices (which would benefit those who intend to upgrade to condos).

The existence of Type B flats will keep Type A flat prices in check, but will not adversely cause a drop in prices for Type A resale flats. As most first timers will choose to go for Type B flats, eventually, the demand for Type A flats will cool, but will not drop adversely there will still be buyers in the form of PRs, 1st timers who can’t afford to wait for a new flat to be build, or current HDB flat owners who wish to move, upgrade or downgrade.

Perhaps down the road, median income will grow at a faster rate, and the gap betweenType A and Type B flats will close up. At that point in time, the classification could be dropped if they no longer serve its purpose.

Of course this is all hypothetical. It may or may not work. Just some thoughts. That’s all.

No comments:

Post a Comment